Form 1099-R Distribution Codes Explained Line by Line

Overview of Form 1099-R Distribution Codes

Updated on March 25, 2024 - 10:30 AM by Admin, TaxBandits

Form 1099-R is used to report passive income, such as annuities or pensions, or distributions made from retirement plans. Individuals managing these plans are mandated to file Form 1099-R for recipients who receive distributions of $10 or more during the calendar year.

However, one of the most difficult parts of reporting Form 1099-R is determining the distribution code that should be entered in Box 7. IRS uses the codes to help determine whether the recipient has properly reported the distribution. If the codes you enter are incorrect, the IRS may improperly propose changes to the recipient's taxes.In this article, we'll break down each code and guide you on which code to include in Form 1099-R.

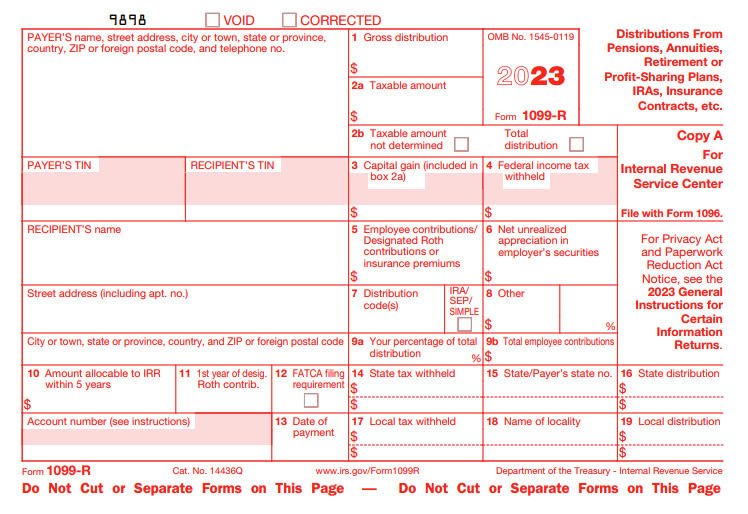

1. What is Box 7 in Form 1099-R?

Box 7 in Form 1099-R is used to identify the type of distribution the recipient received and aids in determining the taxability of the distribution.

There are approximately 29 alphanumeric codes, and you must input the appropriate codes in Form 1099-R. For instance, when utilizing Code P for a traditional IRA distribution under section 408(d)(4), you must also input Code 1 if it applies.

Only two alphanumeric codes can be entered in Box 7 of Form 1099-R. If more than two codes are applicable, two 1099-Rs may be required.

2. Understanding Box 7 Distribution Codes in Form 1099-R

Code 1: Early distribution, no known exception.

Code 1 is used under the following circumstances:

- If the individual is not 59 ½ or older and it is unknown whether any exceptions under expectations in code 2, 3, and 4 apply.

- If the individual is not 59 ½ or older and the distribution is made for any one of the following penalty tax exemptions:

- If the individual modified a series of substantially equal periodic payments before the end of the five-year period that began with the first payment, even if he or she is 59 ½ or older.

Code 1 can be used along with codes 8, B, D, K, L, M, P, if applicable.

Code 2: Early distribution, exception applies.

Code 2 is used only when the individual is under the age of 59 ½ and qualifies for any of the following exceptions:

- If the distribution is made from a Qualified Retirement plan (QRA) or IRA because of an IRS levy under section 6331.

- If the individual directly converted the IRA to a Roth IRA.

- If the distribution is made from a Qualified Retirement plan (QRA) after the participant separated from services during or after the year he or she attained age 55.

- If it's a governmental section 457(b) plans distribution not subject to the additional 10% early distribution penalty tax.

- If a distribution from a governmental defined benefit plan to a public safety employee after separation from service, in or after the year the employee reached age 50.

- If a distribution is part of a series of substantially equal periodic payments, as described in section 72(q), (t), (u), or (v).

- If a distribution is part of a series of substantially equal periodic payments, as described in section 72(q), (t), (u), or (v).

- If an employer matching or nonelective contribution is made to a Roth SEP IRA or a Roth SIMPLE IRA.

- If a distribution is a permissible withdrawal under an eligible automatic contribution arrangement (EACA).

Code 2 can be used along with codes 8, B, D, K, L, M, P (if applicable).

Code 3: Disability

Code 3 is applied if the individual is disabled according to the Internal Revenue Code Section 72(m)(7).

It's important to note that Code 3 should only be used when proof of disability is provided at the time of distribution. The IRS doesn't require verification. However, if no proof is provided, the financial organization should enter Code 1 in Box 7. The individual can still claim the disability exception by filing Form 5329, Additional Taxes on Qualified Plans (Including IRAs) and Other Tax-Favored Accounts.

Code 3 can be used in conjunction with Code D, if applicable.

Code 4: Death

Code 4, is used in the following situations:

- When the distribution is made to the deceased beneficiary, including an estate or trust, following the owner of the retirement plan or plan participant’s death

- If the death benefit payments are made by an employer but not as part of a pension, profit-sharing, or retirement plan.

- When payments are made of reportable death benefits under section 6050Y.

Code 4 can be combined with codes 8, A, B, D, G, H, K, L, M, or P, if applicable.

Code 5: Prohibited transaction

Use code 5 when prohibited transactions involving the IRA account. Which means the IRS tells the IRA is no longer an IRA account.

What Constitutes a Prohibited Transaction in an IRA?

In general, a prohibited transaction within an IRA refers to any improper utilization of an IRA account or annuity by the IRA owner, their beneficiary, or any disqualified person.

Disqualified persons encompass the IRA owner’s fiduciary and members of their family, including their spouse, ancestor, lineal descendant, and any spouse of a lineal descendant.

Code 6: Section 1035 exchange.

Use Code 6 to indicate the tax-free exchange of life insurance, annuity, long-term care insurance, or endowment contracts under section 1035.

Code 6 can be used along with code W (if applicable). .

Code 7: Normal distribution.

Use code 7 for a

- (1) Normal distribution from a traditional IRA, 401(k), and 403(b);

- (2) Roth IRA conversion

- (3) Distribution from a life insurance, annuity, or endowment contract

- (4) Income from a life insurance contract that failed to satisfy the requirements of section 7702.

Please note: Do not use Code 7 for a Roth IRA.

Code 7 can be used along with code A, B, D, K, L, or M (if applicable).

Code 8 - Excess contributions plus earnings/excess deferrals (and/or earnings) taxable in 2024.

Use Code 8 for correction IRS distribution under section 408(d)(4) unless Code P applies. Also you can use code 8 for any excess deferrals, excess contributions, and excess aggregate contributions taxable in the current year, unless Code P applies.

Code 8 can be used along with code 1, 2, 4, B, J, or K (if applicable).

Code 9 - Cost of current life insurance protection

Use code 9 to report the premium paid by a trustee or custodian for current life insurance or other insurance protection plans.

Code A - May be eligible for 10-year tax option.

Use code A only for plan participants born before January 2, 1936, or their beneficiaries to indicate the distribution may be eligible for the 10-year tax option method of computing the tax on lump-sum distributions(on Form 4972, Tax on Lump-Sum Distributions).

It's important to note that determining eligibility for the tax option does not require consideration of whether the recipient previously utilized this method or capital gain treatment.

Code A can be used along with code 4 or 7 (if applicable).

Code B - Designated Roth account distribution.

Use code B for distribution from a designated Roth account. Code A can be used along with codes 1, 2, 4, 7, 8, G, L, M, P, or U (if applicable).

Code C - Reportable death benefits under section 6050Y.

Use code C for the distribution to report payment of the reportable death benefits.

Code C can be used with code D (if applicable).

Code D - Annuity payments from nonqualified annuities and distributions from life insurance contracts that may be subject to tax under section 1411.

Use code D for a distribution from any plan or arrangement not described in section 401(a), 403(a), 403(b), 408, 408A, or 457(b).

Code D can be used with codes 1, 2, 3, 4, 7, or C (if applicable).

Code E - Distributions under Employee Plans Compliance Resolution System (EPCRS).

Use Code -E for distributions under Employee Plans Compliance Resolution System. Code E should not be used with any other codes.

Code F - Charitable gift annuity.

Use Code F if cash or capital gain property is donated in exchange for a Charitable gift annuity.

Code G - Direct rollover and direct payment.

Use code G when:

- A plan participant or IRA owner directly rolls over a distribution from and to an eligible employee qualified plan, a section 403(b) plan, a governmental section 457(b) plan, or an IRA.

- Direct payment from an IRA to an accepting employer plan.

- An In-Plan Roth Rollover (IRR) that is a direct rollover.

Code H - Direct rollover of a designated Roth account distribution to a Roth IRA.

Use Code H when reporting designated Roth account distributions that are directly rolled over to a Roth IRA. Code H may be used in combination with code 4.

Code J - Early distribution from a Roth IRA.

Use Code J, to report a Roth IRA distribution when the IRA owner is under age 59½ and codes Q and T do not apply. Code J can be used with code 8 or P.

Code K - Distribution of traditional IRA assets not having a readily available FMV

Use Code K to report the IRA distribution of an asset that does not have readily available fair market values, such as for the following.

- Stock or other ownership interest in a corporation

- Short- or long-term debt obligations not easily tradable on an established securities market

- Ownership interest in entities like limited liability companies, partnerships, trusts, or similar entities (unless traded on an established securities market)

- Real estate

- Option contracts or similar products not traded on an established option exchange

- Other assets lacking readily available fair market values

Code K must be used along with Codes 1, 2, 4, 7, 8, or G.

Code L - Loans treated as deemed distributions under section 72(p).

Use code L ,when Loans are treated as deemed distributions under section 72(p). Do not use Code L to report a plan loan offset.

Code M - Qualified plan loan offset.

Use Code M for a qualified plan loan offset (which is generally a type of plan loan offset due to severance from employment or termination of the plan).

Code N - Recharacterized IRA contribution made for 2024

Use code N when an IRA contribution is made for 2024 and recharacterized in 2024 to another type of IRA by trustee to trustee transfer or with the same trustee. Code N should not be used with any other codes.

Code P - Excess contributions plus earnings/excess deferrals taxable in 2023.

Use Code P for correction IRS distribution under section 408(d)(4). Also you can use code P for any excess deferrals, excess contributions, and excess aggregate contributions taxable in the current year. Code P can be used along with codes 1, 2, 4, B, or J (if applicable).

Code Q -Qualified distribution from a Roth IRA.

Use Code Q for distributions from a Roth IRA when certain criteria are met. Specifically, it's used when you know that the participant meets the 5-year holding period and is either age 59 1⁄2 or older, has passed away, or is disabled (provided there is proof of disability).

While first-time homebuyer expenses are considered one of the qualified distribution reasons when the five-year waiting period has been satisfied, it's often not known by the distributing organization whether this exception applies. Therefore, code J should be used instead. Code Q should not be combined with any other codes.

Code R - Recharacterized IRA contribution made for 2023.

Use code N when an IRA contribution is made for 2023 and recharacterized in 2023 to another type of IRA by trustee to trustee transfer or with the same trustee. Code N should not be used with any other codes.

Code S - Early distribution from a SIMPLE IRA in the first 2 years, no known exception.

Use Code S if the distribution is from the SIMPLE IRA in the first 2 years, the participant has not reached age 59 ½ and none of the exceptions under section 72(t). Do not use Code S if Code 3 or 4 applies.

Code T - Roth IRA distribution, exception applies

Use code R for distribution from a Roth IRA if you don't know that the participant meets the 5-year holding period and is either age 59 1⁄2 or older, has died, or is disabled (assuming there is proof of the disability).

Note: If any other code, such as 8 or P, applies, use Code J.

Code U - Dividends distributed from an ESOP under section 404(k)

Code U is designated for distributions of dividends from an employee stock ownership plan (ESOP) under section 404(k).

Please note: Dividends paid directly by the corporation to plan participants or their beneficiaries should not be reported here. Those dividends should continue to be reported on Form 1099-DIV. Code U can be used along with Code B (if applicable).

Code W- Charges or payments for purchasing qualified long-term care insurance contracts under combined arrangements.

Code W is used for charges or payments associated with purchasing qualified long-term care insurance contracts under combined arrangements. These charges or payments are excludable under section 72(e)(11) against the cash value of an annuity contract or the cash surrender value of a life insurance contract. Code W can be used along with Code 6 (if applicable).

3. How to file your Form 1099-R with TaxBandits ?

Filing your Form 1099-R with TaxBandits simple and you can file your Form 1099-R in few simple steps

- Select Form 1099-R form the dashboard

- Enter the required information

- Review and transmit your return

- TaxBandits will distribute your recipient via postal mail or online access

Here are some of the benefits you can have by e-filing your returns with TaxBandits:

- TaxBandits supports both Federal and State filing

- Distribute Recipient Copies via Postal Mailing or Go paperless with our Online Access

- Import your data using Excel Templates if you are filing in Bulk

- Ensure accurate filing with Internal Audit Check and TIN Matching

- Get instant help from our dedicated support via Phone, E-mail or Live Chat