Line by line Form 1099-S Instructions

Form 1099-S is used to report real estate transactions. The person or entity responsible for closing the transaction must file Form 1099-S with the IRS and provide copies to the transfereor by the required deadline. In this guide, we will provide step-by-step instructions on how to complete Form 1099-S.

Table of Contents:

What is Form 1099-S?

Form 1099-S is an IRS tax form known as “Proceeds from Real Estate Transactions,” used to report real estate sales or exchanges. This includes sales or exchange for money, property, indebtedness, service, or ownership interest in any

of the following:

- Improved or unimproved land, including air space.

- Permanent structures including residential, commercial, or industrial buildings.

- Condominium unit, including land.

- Stock in a cooperative housing corporation.

- Non-contingent interest in standing timber.

Generally, Form 1099-S is filed by real estate professionals, settlement agents, closing attorneys, escrow companies, and mortgage lenders. This form is filed with the IRS and furnishes recipient copies to the transferors to report the sale proceeds in their personal income tax returns.

What are the new changes in Form 1099-S for the 2025 tax year?

The IRS has updated Form 1099-S for the 2025 tax year to improve accuracy, clarity, and digital asset reporting. Below is a detailed explanation of all the changes made to the form:

-

Address Fields Separated

The Filer’s and Transferor’s address sections are now split into separate fields — including street address, city, state, country, and ZIP code. This update ensures better accuracy and supports the IRS’s new e-filing format.

-

Box 2 — Redesigned for Proceeds Breakdown

Box 2 has been divided into three sub-boxes to provide a detailed breakdown of the types of proceeds:

- Box 2a: Total gross proceeds

- Box 2b: Cash gross proceeds

- Box 2c: Digital asset gross proceeds

This change enables you to accurately report the various types of consideration received in a real estate transaction.

-

Box 6 — Updated for Noncash Consideration

Box 6 now explicitly includes digital assets in addition to services or property as forms of consideration. You must check this box if the transferor received digital assets, property, or services as part of the sale.

-

Boxes 8a–8d — New Digital Asset Reporting Fields

The IRS has added four new boxes (8a–8d) to capture details about digital assets involved in real estate transactions. These are:

- Box 8a: Code for the digital asset received or to be received

- Box 8b: Name of the digital asset (e.g., Bitcoin, Ethereum)

- Box 8c: Number of digital asset units received or to be received

- Box 8d: Date the digital asset was received or will be received

These additions reflect the IRS’s increased focus on digital asset transactions.

How to Fill Out Form 1099-S?

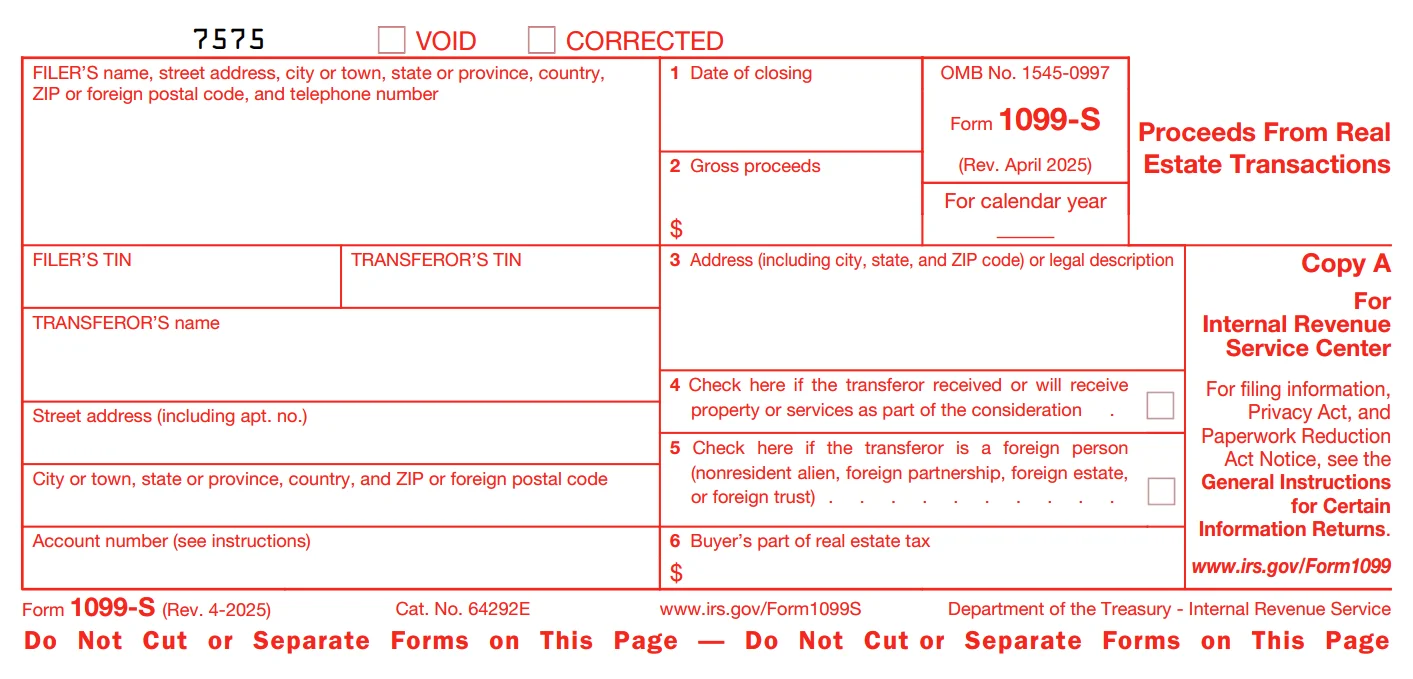

Form 1099-S includes eight boxes, each designed to report specific details about the real estate transaction. Before completing these boxes, the filer must enter their information (name, address, telephone number, and TIN) followed by the transferor’s information (name, address, TIN, and account number if applicable). Once these identification sections are completed, you can proceed to the numbered boxes. Let’s have a closer look at the following table that explains the respective boxes

of Form 1099-S:

| Box No. | Title | Purpose of the Box |

|---|---|---|

| 1 | Date of Closing |

Shows the date when the real estate transaction was finalized. |

| 2a | Total gross proceeds |

The total gross proceeds (generally the sales price) from the transaction. This is the sum of Boxes 2b and 2c, excluding the value of services or property other than digital assets. |

| 2b | Cash gross proceeds |

The portion of gross proceeds received in cash, notes payable, notes assumed by the buyer, or any notes paid off at settlement. Does not include digital assets or other property. |

| 2c | Digital asset gross proceeds |

The gross proceeds received (or to be received) in digital assets, measured in U.S. dollars. A digital asset is any cryptographically secured representation of value recorded on a distributed ledger. |

| 3 | Property address or legal description |

Shows the address (including city, state, and ZIP code) or a legal description of the property transferred. |

| 4 | Buyer’s part of the real estate tax |

The portion of real estate tax charged to the buyer at settlement. This may affect your deductible real estate tax or require reporting as income, depending on prior deductions. |

| 5 | Reserved for future use |

Currently not used by the IRS. |

| 6 | Services or property received |

Checked if the transferor received or will receive services or property (other than cash, notes, or digital assets) as part of the consideration. The value is not included in Boxes 2a through 2c. |

| 7 | Foreign person indicator |

Checked if the transferor is a foreign person (nonresident alien, foreign partnership, foreign estate, or foreign trust). |

| 8a | Digital asset code (DTIF) |

Displays the Digital Token Identifier Foundation (DTIF) code for the digital asset listed in Box 8b. |

| 8b | Digital asset name |

Shows the name of the digital asset received or to be received as consideration. |

| 8c | Number of digital asset units |

Indicates the number of digital asset units received or to be received as consideration. |

| 8d | Date digital asset received |

Shows the date the digital assets were received or will be received as consideration. |

TaxBandits offers secure and accurate filing of 1099 Forms with the IRS. We also provide solutions for distributing your transferor’s copies. E-file Form 1099-S Now.

When is Form 1099-S due?

For the 2025 tax year, the deadline to file Form 1099-S electronically with the IRS is March 31, 2026. In addition to filing Form 1099-S with the IRS, the recipient copy must be furnished to the transferor. The deadline for distributing a transferor copy of Form 1099-S for the 2025 tax year is February 17, 2026.

If you don’t file Form 1099-S within the required deadline, you will be imposed IRS penalties ranging from $60 to $680 per form for the 2025 tax year.

How to File Form 1099-S Electronically?

Once you have all the necessary information, e-filing 1099-S with TaxBandits is simple. Just follow these steps:

- Step 1: Create an account with TaxBandits.

- Step 2: Select or add the business you are filing for.

- Step 3: Enter the required Form 1099-S details.

- Step 4: Review and submit Form 1099-S to the IRS.

Need a recipient copy solution? TaxBandits has you covered! You can select from our postal mail and online access options.

Get started with TaxBandits today and stay compliant with the IRS!

Helpful Resources

What is Form 1099-S?

Form 1099-S Due Date

Form 1099 Correction

Success Starts with TaxBandits

An IRS Authorized E-file Provider You can Trust