Form 941-X: Purpose, Instructions, and Filing Tips

- What is Form 941-X?

- How to correct a mistake on Form 941?

- Are there any changes in Form 941-X for the 2025 tax year?

- What information can be corrected using Form 941-X?

- How to fill out Form 941-X?

- Is it possible to correct errors on Schedule B using Form 941-X?

- When is the deadline for filing Form 941-X?

- How to file Form 941-X?

- Where to mail Form 941-X?

- Are there any penalties related to filing Form 941-X?

What is Form 941-X?

Form 941-X (Adjusted Employer’s Quarterly Federal Tax Return or Claim for Refund) is used to correct any errors made on the 941 Form. If you find an error on a previously filed Form 941, you can correct this error using Form 941-X.

Make sure you file a separate Form 941-X for each tax period only if you have found the errors.

How to correct a mistake on Form 941?

When there is an error on a previously filed Form 941, you can correct the error using Form 941-X.

Criteria for Correcting Form 941-X

You need to file Form 941-X if you meet any of the following criteria:

- Underreported Taxes - This happens when you report less tax than you owe. If you're correcting underreported taxes, you must make a payment when filing Form 941-X.

- Overreported taxes - This happens when you report more tax than you owe. If you're correcting overreported taxes, you can either request a refund or apply the overpayment to your next return.

To claim a refund or reduce the penalty, you can use Form 843 (Claim for Refund and Request for Abatement).

Are there any changes in Form 941-X for the 2025 tax year?

The following changes are made in Form 941-X for 2025:

- Lines 18a, 26a, 30, 31a, 31b, and 32 are now reserved for future use.

- COVID-19-related credit for qualified sick and family leave wages is limited to leave taken after March 31, 2020, and before October 1, 2021, and can no longer be claimed for Form 941.

- Forms 941-SS and 941-PR have been discontinued after the 2023 tax year.

What information can be corrected using Form 941-X?

Form 941-X allows you to correct errors related to wages, employment taxes, tax credits, and other relevant information that was previously reported on IRS Form 941.

The following information can be corrected using Form 941-X:

- Wages, tips, and other compensation

- Income tax withheld from wages, tips, and other compensation

- Taxable social security wages

- Taxable social security tips

- Taxable Medicare wages and tips

- Taxable wages and tips are subject to additional medicare tax withholding

- Qualified small business payroll tax credit for increasing research activities

You can correct the following information for tax year 2023 or earlier, but not for the current tax year:

- Amounts reported on Form 941 for the credit for qualified sick and family leave wages for leave taken after March 31, 2020, and before April 1, 2021, including adjustments to Form 941, lines 5a(i), 5a(ii), 11b, 13c, 19, and 20;

- Amounts reported on Form 941 for the credit for qualified sick and family leave wages for leave taken after March 31, 2021, and before October 1, 2021, including adjustments to Form 941, lines 11d, 13e, 23, 24, 25, 26, 27, and 28;

- Amounts reported on Form 941 for the employee retention credit, including adjustments to Form 941, lines 11c, 13d, 21, and 22; and

- Amounts reported on Form 941 for the COBRA premium assistance credit, for periods of coverage beginning on or after April 1, 2021, through periods of coverage beginning on or before September 30, 2021, including adjustments to Form 941, lines 11e, 11f, and 13f.

You do not need to file a 941-X Form if your errors relate to the number of employees who received wages or Part 2 of Form 941.

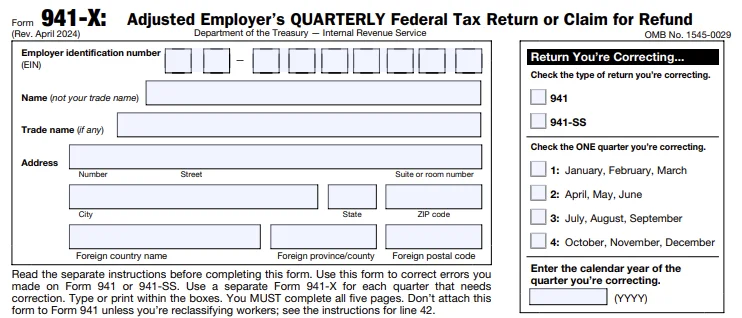

How to Fill Out Form 941-X?

To fill out Form 941-X, follow the step-by-step instructions below:

- Complete the basic information, including your EIN, name, the quarter you are filing for, the company name, and the calendar year.

- Check the appropriate calendar year and the date when you discovered errors.

- Part 1: Choose whether you are correcting the underreported or overreported tax amount. Check the box on line 1 to correct underreported taxes and overreported taxes. You can check the box on line 2 for the claim process.

- Part 2: If the corrections are related to underreported taxes, check Box 3. Lines 4 and 5 are for requesting a refund and reimbursement for the overcollection of taxes from the employees.

- Part 3: Enter the corrections that need to be corrected on the previously filed Form 941.

- Part 4: If any corrections are entered on lines 7- 26c, lines 28 - 31a, or lines 32- 40, you must check the box on line 41. If you have reclassified employees as non-employees, check the box on line 42 and provide the detailed explanation on line 43.

- Part 5: Finally, provide your signature in Part 5.

Click here to get more detailed line-by-line instructions to fill out Form 941-X.

Is it possible to correct errors on Schedule B using Form 941-X?

If you only have errors on Form 941 related to the number of employees who received wages or federal tax liabilities reported in Form 941, Part 2, or Schedule B (Form 941), these cannot be corrected using Form 941-X.

Click here for more information about how to correct Form 941 Schedule B.

When is the deadline for filing Form 941-X?

There is no specific deadline for filing Form 941-X. You must file this form when you find any errors in your previously submitted Form 941. However, a time frame is applicable to report overreported and underreported taxes.

The IRS calls this time frame a “period of limitations.” For the period of limitations, 941 Forms for a calendar year are considered filed on April 15 of the succeeding year, even if they were filed before that date.

- For overreported taxes, you should file Form 941-X within 3 years of the date that the original Form 941 was filed or 2 years from the date you paid the tax reported on Form 941.

- For underreported taxes, you should file Form 941-X within 3 years of the date that the original Form 941 was filed.

How to file Form 941-X?

Form 941-X, filed to correct errors made on Form 941 for tax years before 2024, can only be paper filed and mailed to the IRS. However, starting from the 2024 tax year, the IRS introduced an option to file Form 941-X electronically for quick and secure processing of your amended return. To e-file Form 941-X, you must get started with TaxBandits, an IRS-authorized e-file provider.

Don’t Let Form 941 Mistakes Cost You!

With TaxBandits, you can file Form 941-X quickly, with guided help and no guesswork. Fix errors and stay compliant, on time.

- Late or incorrect filings = IRS penalties.

- Form 941 correction using Form 941-X made simple

- E-file your 941-X in minutes—no paperwork.

In addition, TaxBandits also supports the amendment of Form 941 for tax years 2023 and 2022. You can fill out, review, download, and mail it to the IRS.

Where to mail Form 941-X?

If you choose to mail a paper Form 941-X, send your completed Form 941-X to the mailing address shown in the

table below:

| If you are in | Use this mailing address |

|---|---|

| Connecticut, Delaware, District of Columbia, Florida, Georgia, Illinois, Indiana, Kentucky, Maine, Maryland, Massachusetts, Michigan, New Hampshire, New Jersey, New York, North Carolina, Ohio, Pennsylvania, Rhode Island, South Carolina, Tennessee, Vermont, Virginia, West Virginia, Wisconsin |

Department of the Treasury |

| Alabama, Alaska, Arizona, Arkansas, California, Colorado, Hawaii, Idaho, Iowa, Kansas, Louisiana, Minnesota, Mississippi, Missouri, Montana, Nebraska, Nevada, New Mexico, North Dakota, Oklahoma, Oregon, South Dakota, Texas, Utah, Washington, Wyoming |

Department of the Treasury |

| No legal residence or principal place of business in any state |

Internal Revenue Service |

| Special Filing Addresses for exempt organizations; federal, state, and local governmental entities; and Indian tribal governmental entities regardless of location |

Department of the Treasury |

| If you use a private delivery service to send your Form 941-X from any location to the IRS, it should be delivered to: |

Ogden – Internal Revenue Submission Processing Center

|

Are there any penalties related to filing Form 941-X?

Typically, correcting an underreported amount using Form 941-X will not be subject to penalties or interest if you follow these guidelines:

- File on time (by the due date of Form 941 for the quarter in which the errors are discovered),

- Pay the amount shown on Line 27 by the time you file the Form 941-X,

- Enter the date you discovered the error, and

- Explain your corrections in detail.

You are not eligible to make corrections for interest-free treatment if any of the following apply.

- The underreported taxes are related to an issue raised in an examination of a prior period.

- You knowingly underreported your employment tax liability.

- You received a notice and a demand for payment.

- You received a Notice of Determination of Worker Classification.

Share this article

Need to Amend Form 941? We’re Here to Help!

- File Form 941-X—even if you didn’t file the original 941 with us.

- Step-by-step guidance through the correction process

- Live expert support included

Error?→ Fix → Submit

Related Topics

Related Blogs for Form 941-X

Related Topics

IRS Form 941

- Form 941

- Form 941 Instructions

- Form 941 Due Dates

- Form 941 Mailing Address

- Form 941 Schedule B

- Form 941 Penalty

- Form 941 ERC

- Form 940 vs 941

- Form 941 vs 944

Revised Form 941 for 2023

Form 941 Worksheets

- Form 941 Worksheet 4 for Q3 & Q4 2021

- Form 941 Worksheet 2 for Q2 2021

- Form 941 Worksheet 1

- Form 941 Worksheets

Form 941-X

Revised Form 941 for 2022

Revised Form 941 for 2021

- IRS Form 941 for Q4 2021

- Revised Form 941 for 2nd Quarter, 2021

- Form 941 Quarter 2 vs Quarter 1, 2021

- Revised Form 941 Schedule R for Q2 2021

- Revised Form 941 for 1st Quarter, 2021