Form 8027 Instructions for 2025

This guide provides an overview of Form 8027, including who must file it, the filing deadline, and

step-by-step instructions for

completing the form for the 2024 tax year.

What is Form 8027?

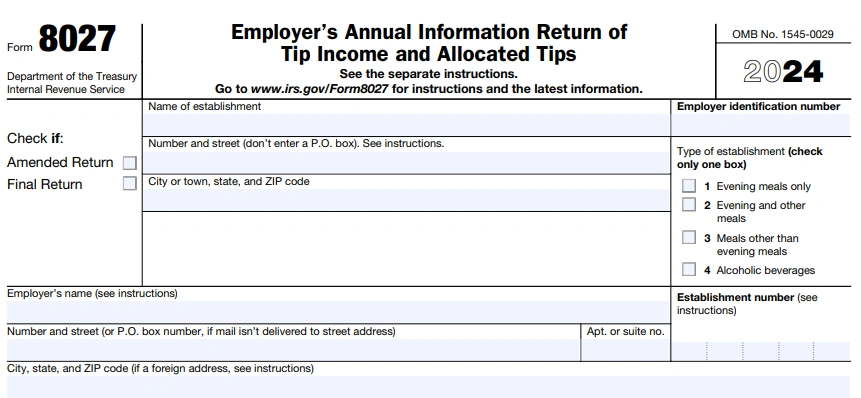

Form 8027, the Employer’s Annual Information Return of Tip Income and Allocated Tips, is used by employers operating food or beverage establishments to report tip income and determine allocated tips for their employees. It ensures compliance with IRS regulations on tip reporting and allocation, facilitating the accurate reporting of employee tip earnings.

-

Indicate the Type of Return

Check the appropriate box to indicate whether you are filing:

- An amended return (if you are correcting a previously filed Form 8027).

- A final return (if your business has closed and will not file Form 8027 again).

-

Establishment Details

- Name and Address of Establishment: Enter the name and address of your establishment. Use the name that customers recognize, such as the name displayed on your building or menu. Also, this address may differ from your (employer’s) mailing address, especially if you own multiple locations.

-

Employer Identification Number (EIN): Enter the EIN assigned to your food or beverage establishment. If you use a Certified Professional Employer Organization (CPEO), refer to IRS guidelines for EIN usage.

Tip: Always use the correct EIN assigned by the IRS. Do not use your Social Security Number (SSN) in place of an EIN.

-

Type of Food or Beverage Establishment: When completing Form 8027, you must select one category that best describes your business. This helps the IRS determine how your establishment reports tip income. Here are the following establishment types:

- Evening Meal Establishment: Serves only dinner (with or without alcoholic beverages).

- Full-Service Meal Establishment: Serves dinner and other meals (breakfast, lunch, or brunch), with or without alcoholic beverages.

- Meals Other Than Evening Meals Establishment: Serves only meals other than dinner (with or without alcoholic beverages).

- Alcohol Beverage Establishment: Primarily serves alcoholic beverages, with food offered as a minor part of the business.

-

Establishment Number: The Establishment Number in Form 8027 is a unique five-digit identification number the employer assigns to distinguish between multiple establishments under the same EIN.

How to Assign an Establishment Number?

- Use a five-digit number to identify each establishment.

- Number them in order, starting with 00001, 00002, etc.

- File a separate Form 8027 for each establishment.

- Keep the same number for each location every year to ensure consistency.

- If you close an establishment, do not reuse its number for a new location.

-

Employer's Details

You must provide the name and address of the business or individual associated with the Employer Identification Number (EIN) you entered earlier. Ensure the following:

- Use the full legal name of the business or individual.

- Enter the complete street address. If mail cannot be delivered to your street address, use a P.O. Box instead.

-

For foreign addresses, include:

- City

- Province or state

- Full country name (Do not use abbreviations).

-

Accepted Payment Methods

You must check “Yes” or “No” to confirm whether your establishment accepts credit cards, debit cards, or other electronic payment methods.

- If you check “Yes” – You must complete Lines 1 and 2 of Form 8027, using the amounts from your charge receipts.

- If you check “No” – You do not need to fill out these lines.

-

Line 1. Total Charged Tips for Calendar Year 2024

- Enter the total amount of tips reported on charge receipts (credit card, debit card, or other electronic payments) for the entire calendar year.

- If your establishment accepts electronic payments but you have no charge tips to report, enter zero.

- Do not include service charges, as they differ from tips. Service charges are pre-determined amounts added to the bill (like for large parties).

Difference Between Service Charges and TipsService charges and tips are treated differently for tax purposes. Service charges are considered wages, and you must withhold federal income, Social Security, and Medicare taxes. These are reported as wages on the employee's Form W-2 and are not listed as tips on Form 8027. You may need to report service charges on line 3 of Form 8027.

A payment is considered a tip if:

- The customer gives it voluntarily, without pressure.

- The customer decides the amount, including the option to give nothing.

- The employer does not set or negotiate the amount.

- The customer chooses who receives the tip.

The payment is likely a service charge if any of these conditions are not met.

-

Line 2. Total Charge Receipts Showing Charged Tips

- Enter the total sales for food and beverages made through charge receipts (e.g., credit card, debit card, or other charges), where a charged tip is shown.

- Don’t include nonallocable receipts, tips, or taxes (state or local) in this total.

- If you indicated that your establishment accepts electronic payments but has no amounts to report here, enter zero.

-

Line 3. Total Amount of Service Charges of Less Than 10% Paid as Wages to Employees

Enter the total amount of service charges (less than 10%) added to customers' bills and distributed to employees during the year. Do not include the tips.

-

Line 4 (a,b,c): Tip Income Reporting Information

Line 4a. Total Tips Reported by Indirectly Tipped Employees

Enter the total amount of tips reported by indirectly tipped employees, such as cooks, bussers, and service bartenders.

Indirectly tipped employees generally receive tips from other tipped employees (e.g., waitstaff) rather than directly from the customer.

Line 4b. Total Tips Reported by Directly Tipped Employees

Enter the total amount of tips reported by employees who are directly tipped, such as waitstaff, bartenders, and maitre d’s.

Directly tipped employees receive tips directly from customers. Even employees like maitre d’s, who may receive tips directly and indirectly through tip splitting or pooling, should be reported as directly tipped employees.

Line 4c. Total Tips Reported (add lines 4a and 4b)

Add the amounts reported in Line 4a (indirectly tipped employees) and Line 4b (directly tipped employees) and enter the result in Line 4c.

The amount reported on Line 4c should not be negative. This is the total amount of tips reported by all employees for the year.

-

Line 5. Gross Receipts From Food and Beverages

On Form 8027, you must report your total gross receipts from food and beverages sold at your establishment. These receipts help determine other required reporting amounts.

What to Include:

Sales of food and beverages, including:

- Cash sales

- Charge receipts

- Charges to hotel rooms (excluding tips if separated in your records)

- The retail value of complimentary food or beverages when tipping is customary

What NOT to Include:

- Tips (unless you subtracted cash paid to tipped employees for charged tips)

- State or local taxes

- Sales of merchandise like souvenirs, memorabilia, tee shirts, or glassware

Special Cases:

- Package Deals: If food and beverages are bundled with other services (e.g., hotel stays), estimate their portion based on cost + a reasonable profit.

- Nonallocable Receipts: Receipts from carryout sales or those with a 10% or more service charge added. Room service is NOT considered carryout.

- Complimentary Items: If tipping is customary and the business is for profit, include the retail value of free food or beverages in gross receipts.

Example: Free drinks in a casino must be included in gross receipts, whereas complimentary appetizers in a bar or desserts for regular customers should not.

-

Line 6. Multiply Line 5 by 8% (0.08) or a Lower Rate

- In line 6, multiply the total gross receipts from Line 5 by 8% (0.08), or if the IRS granted your establishment a lower rate, you should use that rate instead of 8%. In such cases, enter the lower rate and attach a copy of the IRS determination letter to your Form 8027. This calculation is used to determine the portion of gross receipts that is allocated for tips.

- If you have allocated tips for a timeframe other than the calendar year (such as semimonthly, biweekly, quarterly, etc.), mark “X” on line 6 and record the amount of allocated tips (if applicable) from your records on line 7.

The 8% rate (or any lower rate) is used solely for the purpose of tip allocation. This does not imply that directly tipped employees should only report 8% of their tips.

-

Line 7: Allocation of Tips

- If the total reported tips (line 4c) are less than the required amount (line 6), you must allocate the difference (excess tip amount) to employees and report it on line 7 of Form 8027.

- If the reported tips exceed the required amount, no allocation is necessary.

Reporting Allocated Tips on Form W-2: As mentioned earlier, allocated tips should be reported in Box 8 of Form W-2. They don't affect the withholding of income tax, Social Security tax, or Medicare tax, nor are they subject to withholding. Any errors in tip allocation must be corrected using Form W-2c to update SSA records.

Key points to remember:- No Employer Liability for Incorrect Allocations: If you use IRS-approved methods for allocating tips, you aren't liable for mistakes. However, if the allocation on an employee’s Form W-2 is over 5% incorrect, you must correct it.

- Reviewing Other Employees’ Allocations: If you find an error in one employee's tips, review all other employees' tip allocations to ensure fairness.

Methods for Allocating Tips:

Three methods are available when allocating tips to employees. You must check the box on Line 7a, Line 7b, or Line 7c to indicate which method you use for tip allocation.

- Hours-Worked Method: If your establishment has fewer than 25 full-time equivalent employees (tipped and nontipped) per payroll period and the average number of hours worked per business day must be less than 200 hours, then you may use the hours-worked method to allocate tips.

- Gross Receipts Method: If the good-faith agreement method does not work for you, you must use the gross receipts method to allocate tips. Start by calculating 8% of your gross receipts (or a lower approved rate), then subtract tips received by indirectly tipped employees. Distribute the remaining tips among directly tipped employees based on their share of gross receipts, allocate any shortfall accordingly, and report the allocated tips on each employee’s Form W-2.

- Good-Faith Agreement Method: A good-faith agreement method is a written agreement between you and at least two-thirds of tipped employees. It must reflect the actual distribution of tips and take effect by the next payroll period or January 1. The agreement can only be revoked with written consent from two-thirds of the affected employees. Keep a copy for your records.

-

Line 8. Total Number of Directly Tipped Employees

- Enter the total number of directly tipped employees who worked at your establishment throughout the year.

- This is a cumulative total of all employees who received tips directly from customers during the year, even if they only worked a part of the year.

This number should not be used to determine whether or not you must file Form 8027. Refer to the "Worksheet for Determining if You Must File Form 8027" for that information.

-

Signature

Sign your name, provide your title, and enter the date you signed the form. Also, include the best daytime phone number for the IRS to reach you.

Who Must Sign: The person who is authorized to sign for your business entity should sign the 8027 form. This includes,

- Sole proprietorship: The business owner.

- Corporation (including LLCs treated as corporations): The president, vice president, or another principal officer duly authorized to sign.

- Partnership (including LLCs treated as partnership) or unincorporated organization: A responsible and duly authorized partner, member, or officer.

- Single-member LLC classified as disregarded entity for tax purposes: The owner or principal officer duly authorized to sign.

- Trust or estate: The fiduciary.

- Authorized agent: If you have an agent with a valid power of attorney, they can sign on your behalf.

Alternative Signature Methods: Corporate officers or authorized agents can sign Form 8027 by rubber stamp, mechanical device, or computer software program.